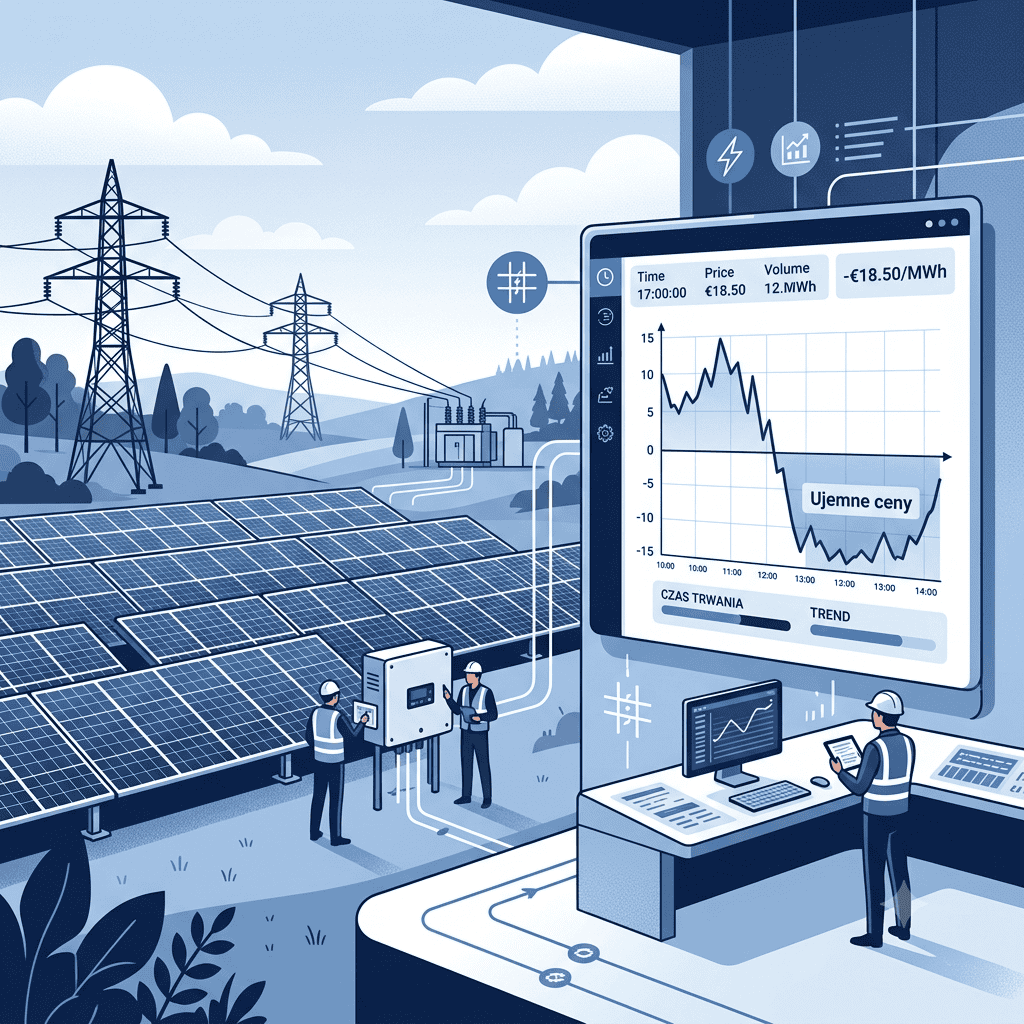

Your Power Purchase Agreement (PPA) says you can zero out during negative prices. Your “Connection Condition” may physically not let you. Your lawyer checked the contract. Nobody checked whether the connection can execute it.

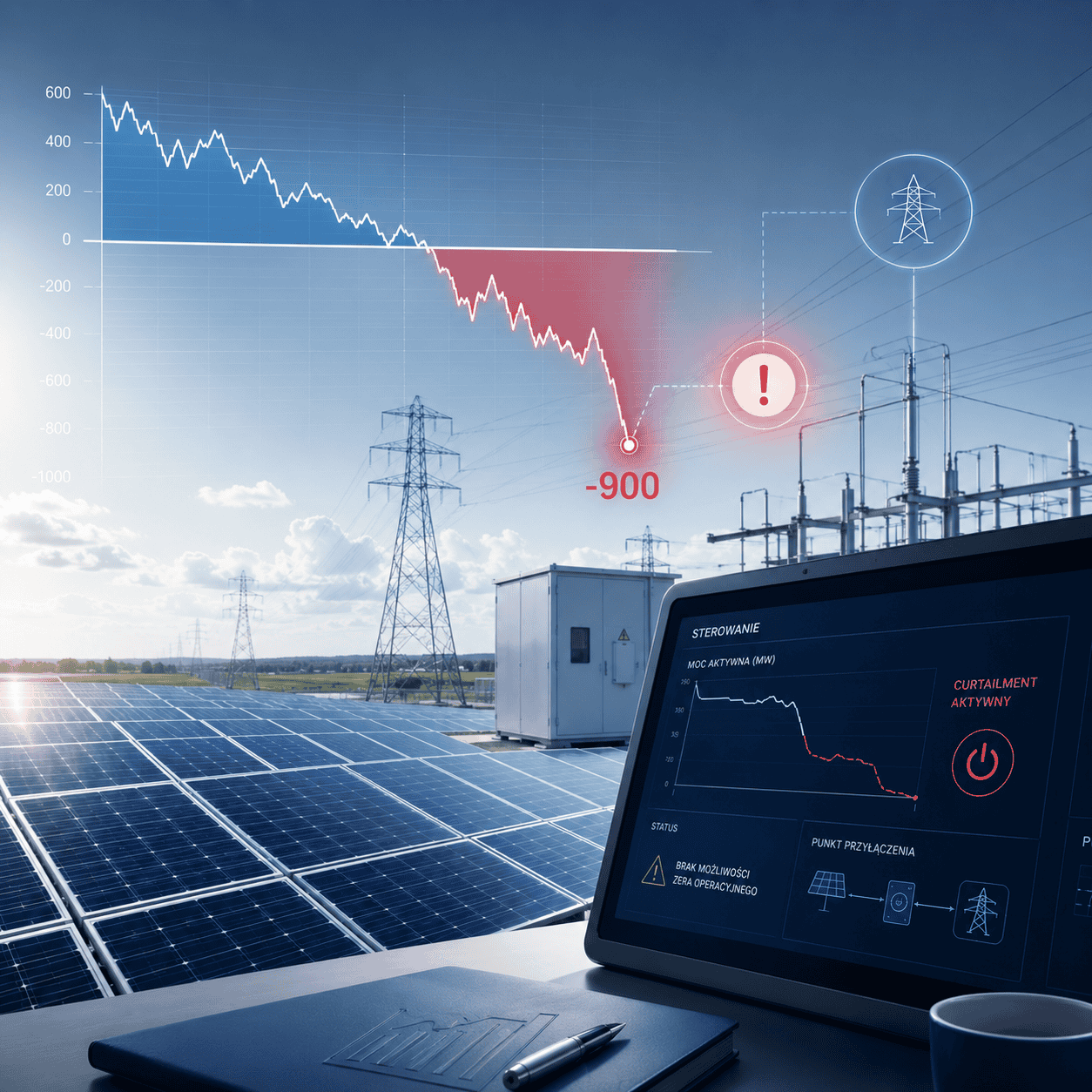

In April 2026, Polish day-ahead prices went negative for dozens of hours, and on 5 April the hourly price fell to minus 900 PLN/MWh. A 50 MW PV farm on a standard pay-as-produced PPA did not simply earn zero in those hours. It ran a balancing deficit, because its Connection Condition could not physically execute the zero-out clause its lawyers had drafted. On paper the documentation was compliant. The physical connection was not, and only one of those facts shows up in a legal review. Nobody flagged it. Not the Distribution System Operator (DSO), not the EPC, not the legal team. GridLink found it during a Connection Condition audit the owner almost did not commission.

In the older Connection conditions we audited through 2025 and 2026, the legal documentation was usually compliant and the physical connection often was not. If your asset was energised years ago, before dynamic active-power control became a standard connection requirement, and your PPA contains a zero-out clause, there is a real chance the two do not match. The right to curtail sits in the contract, and the equipment you actually have cannot carry it out.

Your contract is fighting the grid

Standard Polish PPAs drafted before 2024 rarely include curtailment mechanics that protect the owner during negative-price events, because negative hours were marginal until then. When Polish Power Exchange (TGE) prices fall below zero, Transmission System Operator (TSO) issues non-market redispatch orders, to PV and wind in order to balance the power system. If your PPA does not clearly allocate who absorbs the cost of grid-driven disconnection against the cost of market-driven negative prices, you can end up carrying balancing risk on both at the same time.

There is a second layer. If your Connection Condition were issued years ago, there is a high chance they contain no mechanism for legally suspending generation during hours when the day-ahead price is below zero. Your curtailment right then exists on paper and cannot be executed on the connection.

Your lawyer can draft a zero-out clause. Checking whether your Connection Condition lets you execute it is an engineering and regulatory question, not a legal one, so it falls outside the review you paid for. Your DSO processed your connection. Advising you on whether it holds under the conditions that now apply was never part of that. That read is ours.

A PPA that forces delivery through negative-price hours turns a renewable asset into a recurring liability. A bad negative-price quarter on a highly leveraged asset can wipe out a meaningful share of that year’s equity cash flow and put pressure on debt-service cover, well before it touches the headline revenue line. A Connection Condition audit costs a fraction of the legal fees on the PPA it is meant to protect.

Three clauses that belong in every Polish PPA now

Any fund that bought PV in Germany or the Nordics in the last 18 months already has these flagged in its diligence template. In Polish deals they are still treated as a legal detail, until the first negative-price quarter reaches the Profil and Loss (P&L). If you are selling to institutional capital, refinancing, or closing an acquisition, your Connection Condition curtailment status will be on the other side’s checklist. The only question is whether you find the gap first or they do.

If your contract is missing these, you are already behind

Negative price zero-out (economic curtailment). Automatic suspension of delivery obligations and financial settlement when the day-ahead price stays below zero for a defined consecutive period.

Balancing responsibility demarcation. A clear split of imbalance costs between TSO-ordered non-market redispatch and voluntary economic curtailment. Without it, both can land on the generator.

Co-location and hybrid readiness. An explicit contractual right to retrofit the asset with storage or complementary generation behind the same meter, without reopening the core tariff structure.

Most legal teams will draft these clauses. None of them will tell you whether your physical infrastructure can execute them. That gap is where projects bleed money, and where we work.

The physical bottleneck your legal team cannot see

If a fund is acquiring an older PV asset without a Connection Condition curtailment audit, it is buying a liability priced as an asset. Connections without an executable curtailment mechanism are already drawing valuation discounts before diligence opens. This stopped being a negotiation point. It is now a pricing input.

You cannot simply stop generating if your connection and its control system were never designed for dynamic command. That is the point where the distance between legal strategy and operational reality starts eroding project IRR.

Cable pooling, combining wind, solar, and storage behind a single connection point, is the structural fix. It lets you charge storage during negative-price hours and dispatch when prices recover. Implementing it in Poland means clearing some of the strictest connection rules in Europe. Polish DSOs and TSO require a compliant dynamic active-power control system, a power plant controller that keeps combined output within the contracted connection capacity at every moment.

Hybrid and cable-pooled configurations still have to pass the NC RfG operational notification stages in sequence: energisation (EON), interim (ION), and final (FON). Compliance tests at these stages fail more often than most EPC contractors say upfront, and a failed test leaves your storage idle while negative-price hours keep stacking up on the balance sheet.

| Standard setup | Cable-pooled and compliant |

|---|---|

| PPA: pay-as-produced, full volume risk | PPA: flexible dispatch, zero-out capable |

| Connection: single technology, single limit | Connection: multi-technology, shared capacity |

| Negative-price response: forced generation or unplanned curtailment | Negative-price response: scheduled storage charging, executable curtailment |

| Compliance: standard single-module notification | Compliance: full dynamic active-power control, OSD and PSE approved |

| IRR protection in negative hours: none | IRR protection: structural hedge built into the connection |

Why GridLink, not your lawyer, not your EPC

Your EPC delivered the asset. Your lawyer reviewed the PPA. Neither checked whether your Connection Condition can physically execute the clauses they built, because that question sits between their two mandates. It is an engineering and regulatory read of a legal instrument, and it is the read that decides whether your capital is locked into an asset that performs or one that cannot. In most of the older connections we have audited, that gap was there.

We do not hand you a report full of recommendations. We tell you what is fixable, what is not, and what each path costs. The output is one answer. Your Connection Condition can execute curtailment, or it cannot. If it cannot, you get the cost to fix it and whether the configurable connection agreement route is open with your DSO.

What that means in practice

Connection Condition curtailment audit. You know before you sign the PPA whether you can enforce the zero-out clause, rather than after the first negative-price event.

EON, ION, and FON support for cable-pooled and hybrid configurations, so your storage is not sitting idle through the next negative-price wave.

Power plant controller compliance with DSO and TSO requirements, so your hybrid asset clears certification instead of failing it quietly.

Configurable connection agreement. You adjust your connection terms through the route UC84 actually created, rather than a full reconnection.

The cost of waiting is already moving

April’s losses are already on the balance sheet.

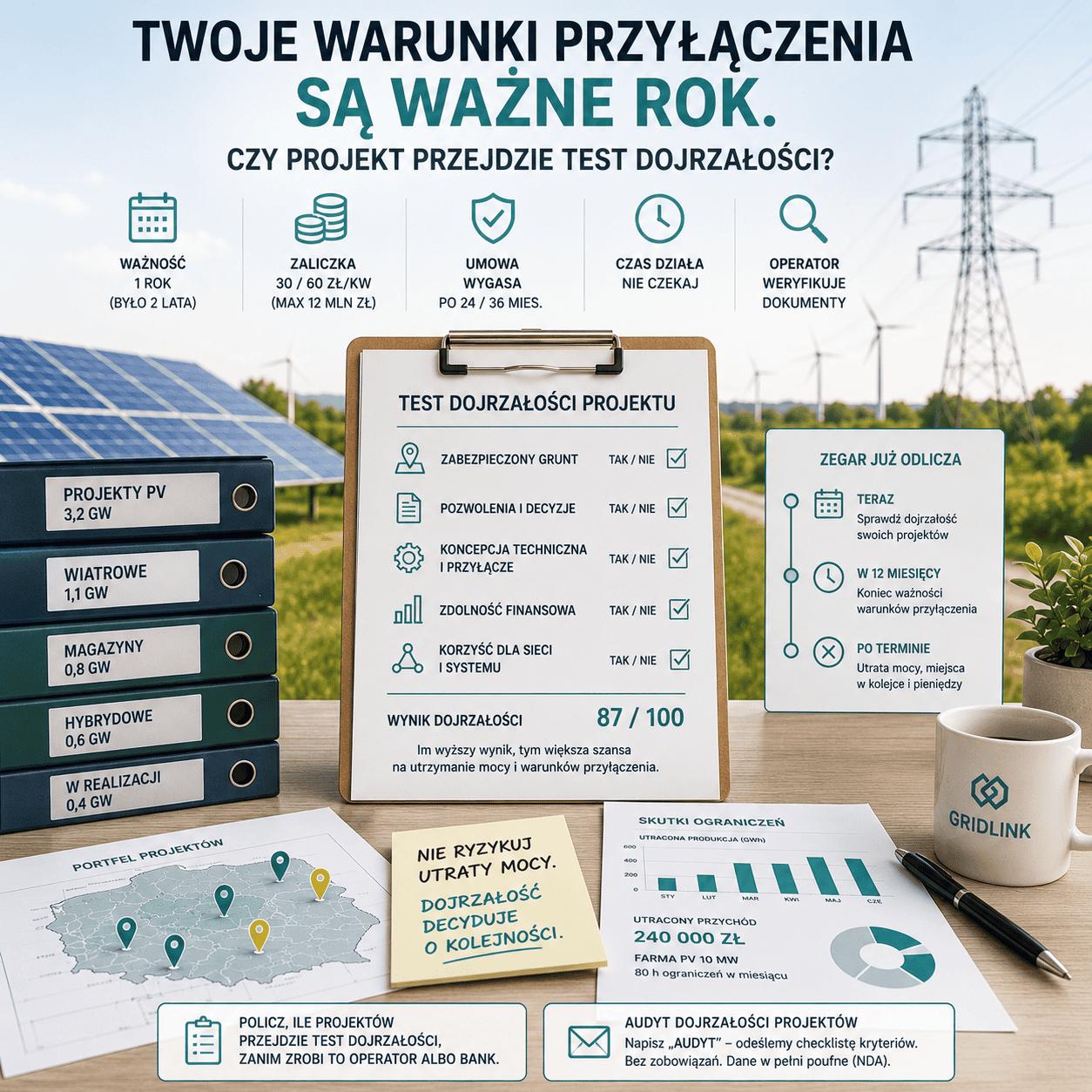

UC84 took effect on 30 April 2026, and it cuts both ways for you. It created the legal vehicle you need, because the new configurable and flexible connection agreements can carry time-variable output limits, which is exactly what a curtailment-capable connection requires. The same law tightened the regime around you. Connection-condition validity dropped to one year, existing projects now run against milestone deadlines for the building permit, and securities have to be topped up on short transition timelines that the market is still arguing over. The tool to fix the mismatch exists today, and the cost of sitting on a connection that cannot execute is climbing on two fronts at once. One is the next negative-price wave. The other is a connection regime that no longer tolerates paper-only positions.

April was not a one-off. TSO’s redispatch data shows non-market curtailment of PV climbing through the summer, with orders issued across multiple days in June. The next wave is not a question of if. The question is whether your connection can do anything about it when it lands.

You probably already suspect which category your asset is in. The only thing left is to confirm it with someone who reads Connection Condition for a living, before a buyer, a lender, or an Limited Partner (LP) does it for you.

Not sure your Connection Condition can execute curtailment?

Send us your Connection Condition document number and connection capacity. Within 48 hours you get one answer, whether your connection supports economic curtailment or not, with the cost to fix it if it does not. No report, no retainer, and what you send stays confidential.

Already holding a Polish PV portfolio you have not stress-tested? We run a limited number of full WP and PPA audits each quarter, and Q3 slots are filling. Book one before the next negative-price wave, not after it shows up in your LP report.